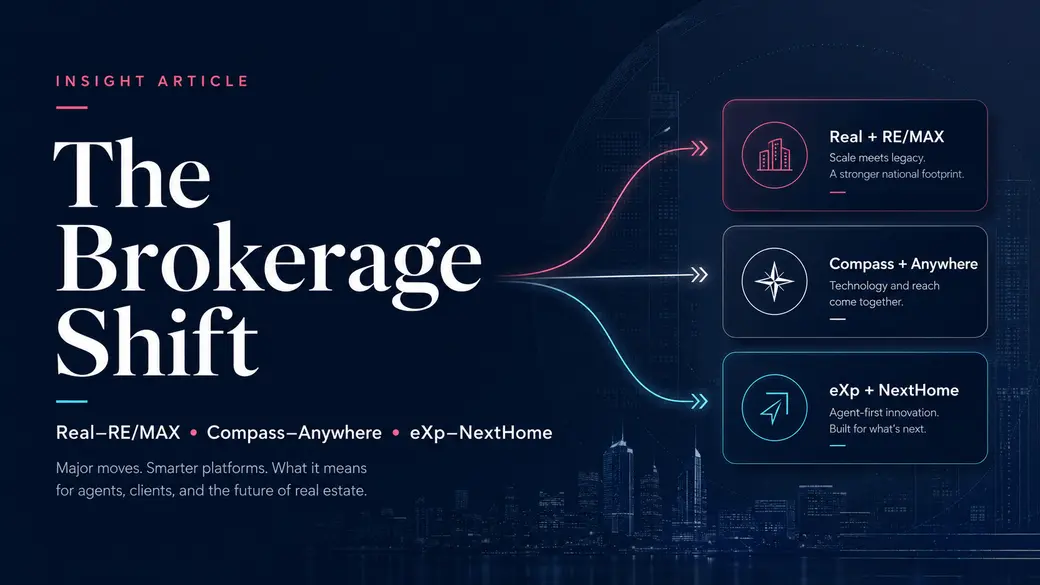

Real–RE/MAX. Compass–Anywhere. eXp–NextHome. The Brokerage Shift.

Three major deals. Fifty years of brokerage history. What do they tell us about where brokerage is headed?

In a short span of time, three major brokerage transactions have created a useful opening to look at where the business may be headed.

Compass completed its combination with Anywhere, bringing several of the industry’s most recognized names — including Coldwell Banker, Century 21, Sotheby’s International Realty, Corcoran, ERA, and Better Homes and Gardens Real Estate — into a larger technology-centered brokerage and services company.

eXp acquired NextHome, adding a national franchise company to a business best known for cloud brokerage.

Real entered into a definitive agreement to acquire RE/MAX, one of the most recognized real estate networks in the world.

These are not the same deal, but they are close enough in timing and direction to raise a fair question:

Why are platform-oriented brokerage companies buying or combining with franchise networks now?

Are they buying agent count? Brand recognition? Local owner relationships? Distribution? Or are these transactions pointing to a larger change in how brokerage companies need to operate?

There is no single answer. But the pattern is worth studying.

To understand what these deals may be telling us, it helps to look at where brokerage came from.

The model that built modern brokerage scale

For decades, franchising was one of the most important ways to scale residential real estate brokerage.

That was not an accident. It solved a real problem.

A local broker-owner could build a company, recruit agents, serve clients, train people, sponsor community events, and create a culture. But building a recognized brand from scratch was hard. So was creating a referral network, training system, national identity, marketing library, business playbook, and recruiting story.

Franchising gave local owners a way to operate independently while connecting to something larger.

Century 21 traces its history to 1971. RE/MAX began in 1973. Keller Williams was founded in 1983 and later grew into one of the most influential franchise systems in the industry. Other national and international brands followed their own paths, building recognition across markets and giving local operators a brand umbrella under which to grow.

For a long time, the practical choices in many markets were fairly simple: join a local independent brokerage, join or open a franchise-affiliated office, or build a local firm around a broker-owner’s own name.

The franchise model fit that era.

Consumers often relied heavily on local signs, office presence, print marketing, relocation relationships, community visibility, and familiar names. Agents often joined offices based on the broker-owner, the local culture, the brand on the sign, the office location, the commission model, and the training environment.

A strong franchise affiliation could give a local owner credibility the first day the office opened. It could help with recruiting. It could create consumer confidence. It could make a local company look larger, more stable, and more connected than it might have looked on its own.

That history matters because the current shift is not a story about old brands having no value. Well-established names like RE/MAX, Coldwell Banker, Century 21, Sotheby’s International Realty, Keller Williams, and others still carry real market equity. Many broker-owners built meaningful businesses with those names. Many agents built careers inside those offices. Many consumers still recognize and trust those brands.

The question is not whether that history matters.

The question is whether the same structure that helped build brokerage scale over the last fifty years is the structure best suited for the next ten.

The industry changed around the model

The brokerage business around the franchise model changed in several ways at once.

Agents became more mobile. Consumers became more digital. Marketing moved from print and office windows to search, portals, social media, video, reviews, email, CRM, and database marketing. Transaction management moved online. Compliance became more system-dependent. Commission processing, agent support, accounting, and documentation became more complex. Recruiting became more competitive. Margins became more sensitive to transaction volume.

The office also changed.

A physical location can still matter. In some markets, a downtown storefront, luxury office, training center, meeting space, or community hub can be a real asset. But the office is no longer the automatic center of brokerage value. Many agents now run much of their business from a phone, laptop, CRM, showing app, digital signature system, cloud document platform, and online marketing stack.

That shift changes the economics of local ownership.

A local office may still be useful. Local leadership may still be essential. Local reputation may still be a competitive advantage. But the broker-owner has to ask whether the entire infrastructure of a local brokerage company still needs to sit underneath that office, that culture, and that leadership.

The pressure is not theoretical.

NAR’s 2025 Profile of Real Estate Firms reported that real estate firms identified housing affordability, industry costs, local economic conditions, and keeping up with technology as leading challenges. Industry costs were cited by 36% of firms, up from 34% in the prior survey. Keeping up with technology was cited by 34%.

NAR also reported that 81% of real estate firms had a single office, with two full-time real estate licensees on average.

That detail matters.

Much of the real estate brokerage industry is still made up of small operating businesses. Many are led by owners who are trying to recruit agents, manage expenses, support transactions, stay compliant, keep technology working, handle staff, and remain profitable in a more difficult market.

The franchise model can provide brand, network, systems, training, and support. But the local owner often still operates a separate local business.

That is where the next model starts to look different.

The rise of platform brokerage

The platform brokerage category is much newer than the franchise era.

eXp launched its cloud-based national brokerage model in 2009. Compass was founded in 2012 and built around a technology-centered agent platform and owned-brokerage model. Real was founded in 2014 as a digital brokerage platform. Other companies, including LPT, Side, Fathom, United Real Estate, and several hybrid or lower-overhead models, have also pushed the industry toward different structures.

These companies are not all the same.

Compass is not Real. Real is not eXp. eXp is not LPT. Side is not Fathom. Each has a different economic model, technology approach, culture, recruiting strategy, ownership structure, and agent value proposition.

But they share a broader idea: brokerage infrastructure can be centralized and scaled.

A franchise affiliation can give a local broker-owner a brand and network. A platform brokerage is designed to provide more of the operating environment itself: technology, transaction workflow, compliance processes, commission processing, reporting, accounting infrastructure, support, data, and the ability to operate across markets without recreating the brokerage infrastructure in every location.

That does not make one model morally better than the other. It does mean they solve different problems.

Franchising solved the problem of local credibility and repeatable brand expansion. Platform brokerage is trying to solve the problem of operating leverage, and that has become one of the most important issues in real estate brokerage.

Where the growth has moved

A serious analysis has to separate market presence from market momentum.

The franchise footprint remains large. NAR’s 2025 Residential Franchise Report noted that 38% of NAR members were affiliated with a franchise company in 2012. After small fluctuations over the years, the figure was still 38% in 2025.

That is important, but it also says something else: by that measure, franchise affiliation has not grown in thirteen years.

That does not mean franchise-affiliated offices have no value. Well-established brands, local offices, broker-owner relationships, agent comfort, community presence, and referral networks do not disappear overnight.

But where the growth is happening tells a different story.

Recent rankings and industry data show much of the momentum moving toward platform-oriented or lower-overhead brokerage models.

RealTrends’ 2026 rankings, based on 2025 production, showed Compass as the top brokerage by sales volume and eXp as the top brokerage by transaction sides. The same rankings showed Real and LPT moving up meaningfully in the national brokerage picture.

T3 Sixty’s 2026 Real Estate Almanac adds another layer. Among the largest U.S. real estate enterprises, Real showed 53.7% year-over-year sales volume growth from 2024 to 2025, 45.1% transaction-side growth, and 20.6% agent-count growth. LPT showed 70.4% sales volume growth, 67.8% transaction-side growth, and 43.6% agent-count growth. Compass showed 15.6% sales volume growth, 10.3% transaction-side growth, and 16.5% agent-count growth.

At the same time, several of the largest legacy franchise systems showed agent-count declines in the same Almanac data. Keller Williams was down 5.9% in U.S. agent count. Coldwell Banker was down 3.0%. RE/MAX was down 6.1%. Century 21 was down 4.5%. Berkshire Hathaway HomeServices was down 11.4%.

Those numbers do not tell the whole story. One year of data should not be treated as destiny. eXp, for example, remained one of the largest brokerage enterprises in the country by transaction sides even while showing a modest year-over-year decline in some Almanac measures. Some established names may lose agent count while improving productivity, volume, margin, or market focus. Some platform models may grow quickly and still have their own financial, cultural, or operational challenges.

Still, the pattern is meaningful.

The broad franchise affiliation number has been flat. The recent growth story has been increasingly associated with platform-oriented and lower-overhead models.

That is the tension behind the current wave of transactions.

What the three deals may be signaling

The three transactions should not be treated as identical. They are different deals involving different companies.

But they are useful because each reveals a piece of the larger shift.

Compass–Anywhere

The Compass–Anywhere combination is the largest and broadest example.

Anywhere brought a massive collection of real estate assets: company-owned brokerage operations, franchise networks, relocation, title, escrow, and some of the most recognized names in residential real estate. Compass brought a modern brokerage platform, a strong acquisition and recruiting track record, a proprietary technology story, and a strategy focused on building a larger end-to-end real estate services company.

After the deal closed, Compass said its technology would be branded as the Home Platform and that it expected to make it available to Anywhere’s company-owned brokerage agents in 2026, with plans to roll it out to the franchise network in 2027.

That detail is important.

Compass did not simply acquire a collection of names and leave the operating question untouched. The stated integration path involves bringing a legacy brand-and-services portfolio onto a broader technology platform.

That is not the disappearance of established brand equity. It is the attempt to connect established brand equity to a larger operating system.

eXp–NextHome

The eXp–NextHome transaction is different, and that difference is useful.

NextHome was not publicly positioned as a distressed legacy system. It had a modern brand, a national footprint, and a strong reputation among franchise owners. eXp described the acquisition as creating a unified platform for both franchise and cloud brokerage models, offering real estate professionals a choice between franchise ownership and cloud-based models.

That suggests a future where the industry is not divided neatly into old versus new.

A company can support more than one model. A franchise path can exist inside a platform company. A cloud brokerage can own a franchise network. A platform can become an umbrella for multiple forms of entrepreneurship.

That may be one of the clearest signals in the market.

The next era may not be one model replacing every other model. It may be the consolidation of multiple models under larger infrastructure companies.

Real–RE/MAX

The Real–RE/MAX agreement is the most directly relevant transaction for RE/MAX broker-owners because it puts a long-established franchise network next to a fast-growing platform brokerage inside one proposed corporate structure.

Real announced that it had entered into a definitive agreement to acquire RE/MAX Holdings to create Real REMAX Group. The announcement described the transaction as combining Real’s AI-powered, high-growth brokerage platform, proprietary software, and agent community with RE/MAX’s global reach and franchise network.

The release also stated that RE/MAX and Motto Mortgage would continue to operate under their current brands, while Real would continue to operate as an owned brokerage under the Real brand.

That means the public message is continuity. No serious analysis should imply that RE/MAX disappears, that franchise agreements automatically change, or that broker-owners should make assumptions about their legal obligations.

But the strategic message is still significant.

Real’s transaction materials say franchisees are expected to benefit from stronger agent attraction and retention, expanded revenue opportunities, and lower operating costs while maintaining their existing business model and brand identity. The same materials refer to streamlined back-office operations, reduced reliance on multiple third-party vendors, and improved transaction management, compliance, and workflow efficiencies over time.

That is the language of a platform company looking at a franchise network and saying: the brand and relationships matter, but the operating system underneath them matters too.

The real pressure point: who owns the infrastructure?

This is where the discussion becomes most important for broker-owners.

A local franchise owner may have a respected brand, strong agents, community presence, and a real leadership role in the market. But that same owner may still carry the infrastructure of a separate operating company: E&O insurance, compliance workflow, document storage, transaction management, commission processing, accounting, office leases, payroll, HR, staff management, local marketing, software subscriptions, vendor contracts, tax reporting, claims management, recruiting costs, training costs, and local profitability risk.

Some of those costs are visible. Others are hidden in time, complexity, and management attention. The visible cost might be a franchise fee, technology fee, marketing contribution, annual due, or office lease. The hidden cost is the owner’s day.

Who fixes the software problem? Who reconciles the commission question? Who handles the compliance issue? Who deals with the staff problem? Who reviews the insurance policy? Who worries about the lease? Who answers the accounting question? Who makes sure the local system and the franchise system and the transaction system and the document system and the accounting system all agree?

A national platform has a different economic premise. It can spread infrastructure across thousands or tens of thousands of agents. It can invest once and deploy broadly. It can standardize workflows. It can centralize support. It can build or integrate systems with a much larger user base in mind.

Better technology helps, but it does not automatically solve the local-owner problem. If the local office remains a separate operating company, the owner may still have separate accounting, separate payroll, separate staff, separate E&O, separate leases, separate vendor contracts, separate tax issues, separate compliance execution, and separate local risk. The technology stack may improve, but the owner is still running the local business.

That is the difference between adding technology to a local business and moving more of the business onto a platform.

This is the core question: if the local owner’s highest value is leadership, recruiting, coaching, culture, agent development, and local market knowledge, does that owner still need to own every layer of brokerage infrastructure?

The cost model under pressure

The economics of brokerage have always been sensitive to volume. When transaction volume is high, inefficiency can hide. When markets slow, every layer becomes more visible: office space, staff, software, insurance, compliance, recruiting, accounting, marketing, and franchise fees.

Brokerage is not operating in a frictionless environment. Housing affordability is strained. Inventory has been uneven. Mortgage rates changed consumer behavior. Agent count has been pressured in many places. Recruiting is harder. Experienced agents are comparing economics more aggressively. Technology expectations keep rising.

In that environment, local ownership cost becomes a strategic issue.

A franchise owner may still have a brand that agents respect. They may still have a culture agents love. They may still have training, local leadership, and community presence. But if the local owner is carrying a cost structure that a national platform can spread across a much larger base, the comparison becomes harder.

The owner is not just competing against another office across town. They are competing against companies that may be able to centralize technology, accounting, transaction management, compliance workflow, support, AI, data, and expansion infrastructure across many markets at once.

The office fits into that same discussion. A productive office, training hub, client meeting space, luxury presence, downtown storefront, or regional collaboration center can still be valuable. But an office is no longer automatically the operating center of the business. It has to prove its role more clearly.

That does not mean offices disappear. It means the office becomes a strategic tool, not the reason the whole brokerage infrastructure has to remain local.

This may explain why the current acquisitions feel like more than ordinary consolidation. They may reflect a recognition that brokerage scale is no longer just about how many signs are in a market. It is about how much operating infrastructure can be shared across the organization.

What RE/MAX owners should be watching

For RE/MAX broker-owners, the Real–RE/MAX agreement brings this discussion closer to home.

The transaction has not closed as of this writing. It remains subject to customary closing conditions, regulatory approvals, and shareholder approvals. The public transaction materials state that RE/MAX and Motto Mortgage will continue under their current brands, while Real will continue under the Real brand.

So no one should overstate what has happened.

The agreement does not automatically change a franchise owner’s contract. It does not tell any owner what to do. It does not eliminate the need to review agreements, state law, licensing obligations, leases, vendor contracts, staff issues, financials, tax implications, or professional responsibilities with qualified advisors.

But it does change the strategic context.

If RE/MAX becomes part of a larger organization that also includes Real’s national brokerage platform, RE/MAX owners will have reason to understand both models more deeply.

The useful question is not, “Should I react immediately?”

The useful questions are more disciplined:

- What does my current structure cost me in money, time, complexity, and risk?

- Which parts of my business do my agents actually value?

- Is my brand value local, national, personal, or some combination of all three?

- Do my agents stay because of the name, because of my leadership, because of the culture, because of the economics, because of the tools, or because of habit?

- Could my organization grow faster if it did not have to recreate brokerage infrastructure market by market?

- Could I support agents across more geographies if the licensing, compliance, transaction, and accounting backbone were already in place?

- Could I spend more time recruiting, coaching, training, and leading if less of my energy went into back-office ownership?

Those questions do not require an immediate answer. But they are the questions serious owners should be asking.

They also lead to a more personal question for any broker-owner: what exactly are you trying to protect?

Broker-owners who built local companies deserve respect. They took risk. They recruited agents. They signed leases. They built culture. They handled problems agents never saw. They carried compliance, staff, risk, and overhead. They created something real.

But the irreplaceable value may not be the lease, payroll system, accounting stack, compliance workflow, E&O policy, document storage, local software bundle, and administrative machinery. The irreplaceable value may be the leadership, culture, coaching, agent relationships, recruiting ability, local reputation, and ability to help people succeed.

Most great broker-owners did not get into ownership because they loved payroll, E&O renewals, commission reconciliation, software integrations, compliance files, tax questions, or vendor management. They became owners because they wanted to lead.

If a local owner can preserve leadership, culture, agent support, training, recruiting, local identity, and growth strategy while reducing the burden of infrastructure ownership, the owner may become more valuable to the agents, not less.

That may be the real opportunity in the brokerage shift.

What the next ten years may look like

No one can predict the brokerage industry with certainty.

Real estate is local. Relationships matter. Interest rates matter. Inventory matters. Commission pressure matters. Regulation matters. Capital markets matter. Technology changes quickly. Consumer behavior changes unevenly. Some local companies will keep thriving because they are well run, deeply trusted, and financially disciplined.

Still, the direction of travel is becoming easier to see.

Well-established names like RE/MAX, Coldwell Banker, Century 21, Sotheby’s International Realty, Keller Williams, and NextHome still carry real equity. That equity was built over decades, and it will not simply vanish.

But the infrastructure underneath brokerage appears to be moving toward larger platforms.

Some franchise systems may become more platform-enabled, giving owners better technology, better transaction workflow, more centralized support, and access to broader services. Some platform companies may continue buying or combining with established networks because those networks provide distribution, relationships, geography, and brand recognition. Some broker-owners may keep their existing structure and become more efficient inside it. Others may move their local organizations onto national platforms while preserving leadership, culture, local identity, and agent support in a new form.

The common thread is not that local leadership goes away. The common thread is that local leadership may increasingly be supported by national infrastructure.

That is the brokerage shift.

The old question was often: which brand should I affiliate with?

The newer question may be: what should my business run on?

The recent transactions do not answer the future by themselves, but they do create a useful lens. Compass–Anywhere suggests that established names and services can be pulled into a larger technology and brokerage ecosystem. eXp–NextHome suggests that cloud brokerage and franchise ownership can sit inside the same corporate platform. Real–RE/MAX suggests that a global franchise network and a fast-growing digital brokerage platform may be viewed as complementary rather than separate worlds.

Taken together, these deals point toward a brokerage industry where brand, leadership, technology, infrastructure, and scale are being recombined.

For broker-owners, the issue is not whether their local leadership still matters. It does. The issue is whether the structure underneath that leadership still gives agents the best chance to grow.

A local owner who recognizes this shift early may not lose stature. They may gain it. Agents respect leaders who see around corners. They respect leaders who make hard decisions before the market makes those decisions for them. They respect leaders who protect the future of the organization, not just the familiar shape of the past.

The real estate franchise model helped build one era of brokerage scale. The platform model is building the next one.

The owners best positioned for what comes next may be the ones who understand both — and who are willing to ask the hardest question before everyone else does:

What structure gives my agents the strongest future, and gives me the best ability to lead them?

What changed when I moved my brokerage onto a platform

I am not looking at this shift only as an observer. I lived a version of it.

Before leading ProAgent at Real, I operated my own brokerage business. As the company grew, the work of ownership changed. More and more of my time went into managing the machinery of the brokerage: employees, compliance, accounting, software, document storage, commission processing, insurance, payroll, systems, and the general operational weight that comes with running a brokerage company.

Those things mattered, and they had to be done well. But they were not the reason I got into brokerage leadership.

I wanted to build relationships with agents. I wanted to coach, mentor, recruit, solve problems, help people grow, and create an environment where agents could do better work. As the brokerage became larger, I found myself spending less time in those relationships and more time managing the infrastructure around them.

Moving the business onto Real’s platform changed that.

The biggest benefit was not simply a different brand or a different compensation model. It was the ability to stop carrying so much of the local brokerage infrastructure myself. Compliance workflow, document storage, transaction systems, accounting complexity, back-office software, commission processing, and many of the staff-heavy administrative functions moved into a larger platform structure.

Real had already built the systems, policies, and ProTeams software that made that kind of move practical. A brokerage-minded leader can bring an existing operation onto the platform, preserve much of the local leadership, culture, support model, and agent relationships that made the business valuable, while taking advantage of the infrastructure Real has already created.

That is the important distinction. The goal is not to erase what made the local organization work. The goal is to keep the best parts — leadership, relationships, coaching, recruiting, support, and culture — while removing more of the operational drag that kept the owner buried in back-office work.

That gave me more time to be in direct relationship with agents again. More phone calls. More coaching. More mentoring. More practical conversations about their business. More of the work I actually believed made me valuable as a leader.

That experience is why I see these industry transactions as more than corporate news. For broker-owners, the question is not only what company owns what brand. The question is whether the structure underneath the business still supports the work the owner is best suited to do.

This article is not legal, financial, tax, franchise, or investment advice. Broker-owners should review their own franchise agreements, state rules, licensing requirements, leases, vendor contracts, financials, and professional obligations with qualified advisors before making any decision.

Recent Posts